On March 16, 2022, the Federal Reserve Bank announced that it would raise interest rates for the first time since December 2018. On the surface, the resulting 25 basis point hike didn’t seem like much. But the hike signals a shift in the commercial real estate landscape—one that investors are watching closely.

Rising Interest Rates – What This Really Means

First, a quick primer on interest rates: when someone refers to the Fed increasing the interest rate, this really means that the rate to borrow federal funds is increasing. In theory, this does not impact consumers directly. Instead, the target federal funds rate is the rate at which banks borrow reserve balances from one another. In practice, however, this trickles down to impact consumers.

When the federal funds rate increases, it becomes more expensive for banks to borrow the money they need to make large commercial loans. Therefore, it eventually becomes more expensive for borrowers seeking CRE loans to construct, acquire, or refinance commercial property.

As the cost of capital increases, this has ripple effects throughout the industry (which we’ll explore in more detail below).

Why Interest Rates are Rising

Historically, interest rates are correlated with inflation. For example, when the housing market collapsed in 2008 and during the subsequent recession, the federal government slashed interest rates. Doing so was an attempt to stimulate the economy. While it worked, we all know for every action there is an equal and opposite reaction. And in the case of the economy, the free flow of money into the system tends to create inflation (which impacts everyone – particularly the everyday citizen), plus the significant increase in the national debt.

Interest rates continued to hover around near-record lows until 2018 when, faced with a surging economy, the Federal Reserve began gradually increasing the rate. However, the COVID-19 pandemic put further interest rate hikes on hold over fears of another economic recession. The continued low-interest-rate environment helped to bolster the economy during a period of uncertainty.

Now, as the economy bounces back following the shutdowns brought on by the COVID-19 pandemic, the Fed is increasing rates yet again in an attempt to combat surging inflation. As of February 2022, annual inflation was up 7.9 percent—a 40-year high. See our recent article how inflationary environments impact CRE investors and owners.

The 25-basis point increase (0.025 percent) in March is just the first of what many expect to be several interest rate hikes this year. Last month, a survey of Federal Open Market Committee (FOMC) members indicated that they expected interest rates to rise another 1.875 percent by the end of 2022. They projected the federal target rate could increase to as much as 2.8 percent in 2023 before flattening out. Again, the goal is to combat inflation. FOMC members indicated that the interest rate would need to rise by this amount to stabilize inflation to closer to 2-3 percent per year.

How Rising Rates Impact CRE

Nearly all commercial real estate is purchased using some combination of debt and equity. Therefore, rising interest rates can dramatically impact the cost of real estate. In short, as the cost of capital rises, it becomes more expensive to own real estate—all else considered equal.

Let us put that in perspective. Every 25-basis point increase equates to an extra $25 per year in interest on $10,000 worth of debt. On a $10 million loan, this means an additional $25,000 per year in interest. If interest rates were to rise by 2.8 percent, this equates to an additional $280,000 per year in interest.

As you can imagine, a sharp rise in interest rates can quickly eat into an investor’s cash flow. Worse, some projects may no longer pencil out to be profitable and ultimately curb growth.

Here’s a more comprehensive look at how rising interest rates impact commercial real estate:

- Prices may come down. In recent years, CRE assets have been trading at all-time highs. It was not uncommon to see deals trading at or below a 3-cap, depending on property type and market. In a low-interest-rate environment, investors are willing to pay more for an asset. As interest rates rise, investors need to pay less for the property to achieve the same numbers. This can have a cooling effect on the market.

- Transaction activity may slow. As interest rates rise, some would-be buyers will remain on the sidelines, afraid of overpaying for a property given the high cost of debt. Meanwhile, would-be sellers may decide to hold off on selling until market conditions once again improve in their favor.

- Investors may look elsewhere. With interest rates on the rise, investors will begin looking at their alternatives. In an inflationary environment, some deals may not offer a compelling risk-adjusted return relative to other investments. For example, one consequence of rising inflation is that the yields on U.S. Treasury bonds are increasingly rising. Properties that were trading at a 3-cap become less compelling if the rate on 10-Year Treasury bonds is 2.5 percent, which they are today. In other words, the risk-adjusted returns on CRE should be higher than other investment types. If higher interest rates mean they are not, some people may decide to invest elsewhere until conditions change. The flip side of this is that the 2.5 percent “risk free rate” of a 10-Year Treasury bond does not offer any upside or future appreciation, while solid long term real estate deals operated by experienced managers can still offer upside. This is particularly the case in a high interest rate environment in which rents on multifamily assets generally benefit from inflation.

Should CRE Investors Panic? No – At Least, Not Yet.

While CRE investors should certainly monitor the interest rate environment, it is important to understand that the Federal target rate is not the be all, end all.

In fact, many would argue it’s the wrong indicator to be following. Instead, investors should be paying close attention to what’s happening to yields on 10-Year U.S. Treasuries.

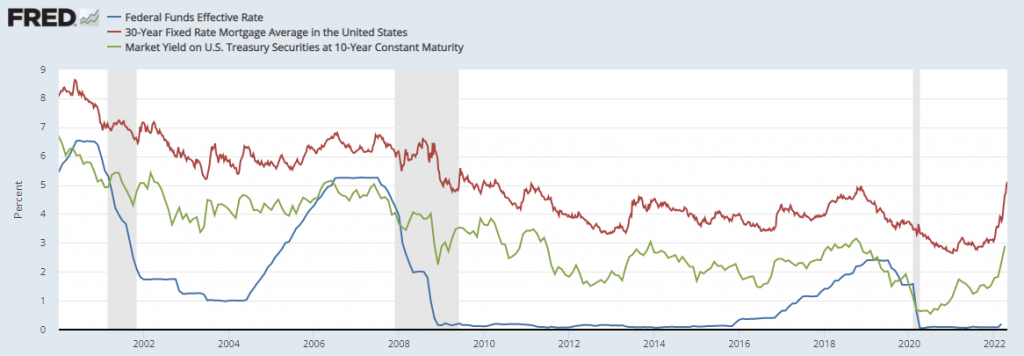

The chart below highlights how changes in the Fed’s target rate (the blue line) don’t actually have a dramatic impact on mortgages (red line). Instead, there is a stronger correlation between the yields on 10-Year Treasures (green line) and mortgages.

The yield on Treasuries is certainly influenced by the Fed’s target rate, but it is also influenced by other factors such as the stock market and geopolitical events (e.g., the war in Ukraine). Given today’s economic and political environment, it would not be a surprise to see Treasury yields increase further, therefore pushing mortgage rates up in turn.

That said, interest rates, though they are on the rise, remain dramatically lower than they were in decades past. Using the same chart above, we can see that mortgage interest rates were close to 9 percent in the early 2000s. And remember, mortgage interest rates were upwards of 18 percent in the early 1980s. We are nowhere close to that, even if interest rates “rapidly” rise.

Some sectors, such as multifamily, will continue to outperform other asset classes even amid rising interest rates. Any downward pressure caused by rising mortgage rates should be counteracted by unfettered demand for housing. Investors continue to pour record amounts of capital into multifamily and for now, this shows no signs of slowing down. Rising interest rates are generally correlated with improving economic conditions, and as the economy improves, landlords will be able to push rents to combat higher priced debt. Meanwhile, office, retail, and hospitality properties will be bolstered by a generally improving economy.

While the Fed’s interest hikes certainly draw a lot of attention, it is important to put this news in the context of other market factors driving the CRE landscape. On the whole, the CRE market remains strong. At HLC Equity, we continue to pay close attention to the debt markets as interest rates rise and act defensively to preserve our investors’ capital. Interested in learning more? Contact us today.