On March 16, 2022, the Federal Reserve Bank announced that it would raise interest rates for the first time since December 2018. On the surface, the resulting 25 basis point hike didn’t seem like much. But the hike signals a shift in the commercial real estate landscape—one that investors are watching closely.

Rising Interest Rates – What This Really Means

First, a quick primer on interest rates: when someone refers to the Fed increasing the interest rate, this really means that the rate to borrow federal funds is increasing. In theory, this does not impact consumers directly. Instead, the target federal funds rate is the rate at which banks borrow reserve balances from one another. In practice, however, this trickles down to impact consumers.

When the federal funds rate increases, it becomes more expensive for banks to borrow the money they need to make large commercial loans. Therefore, it eventually becomes more expensive for borrowers seeking CRE loans to construct, acquire, or refinance commercial property.

As the cost of capital increases, this has ripple effects throughout the industry (which we’ll explore in more detail below).

Why Interest Rates are Rising

Historically, interest rates are correlated with inflation. For example, when the housing market collapsed in 2008 and during the subsequent recession, the federal government slashed interest rates. Doing so was an attempt to stimulate the economy. While it worked, we all know for every action there is an equal and opposite reaction. And in the case of the economy, the free flow of money into the system tends to create inflation (which impacts everyone – particularly the everyday citizen), plus the significant increase in the national debt.

Interest rates continued to hover around near-record lows until 2018 when, faced with a surging economy, the Federal Reserve began gradually increasing the rate. However, the COVID-19 pandemic put further interest rate hikes on hold over fears of another economic recession. The continued low-interest-rate environment helped to bolster the economy during a period of uncertainty.

Now, as the economy bounces back following the shutdowns brought on by the COVID-19 pandemic, the Fed is increasing rates yet again in an attempt to combat surging inflation. As of February 2022, annual inflation was up 7.9 percent—a 40-year high. See our recent article how inflationary environments impact CRE investors and owners.

The 25-basis point increase (0.025 percent) in March is just the first of what many expect to be several interest rate hikes this year. Last month, a survey of Federal Open Market Committee (FOMC) members indicated that they expected interest rates to rise another 1.875 percent by the end of 2022. They projected the federal target rate could increase to as much as 2.8 percent in 2023 before flattening out. Again, the goal is to combat inflation. FOMC members indicated that the interest rate would need to rise by this amount to stabilize inflation to closer to 2-3 percent per year.

How Rising Rates Impact CRE

Nearly all commercial real estate is purchased using some combination of debt and equity. Therefore, rising interest rates can dramatically impact the cost of real estate. In short, as the cost of capital rises, it becomes more expensive to own real estate—all else considered equal.

Let us put that in perspective. Every 25-basis point increase equates to an extra $25 per year in interest on $10,000 worth of debt. On a $10 million loan, this means an additional $25,000 per year in interest. If interest rates were to rise by 2.8 percent, this equates to an additional $280,000 per year in interest.

As you can imagine, a sharp rise in interest rates can quickly eat into an investor’s cash flow. Worse, some projects may no longer pencil out to be profitable and ultimately curb growth.

Here’s a more comprehensive look at how rising interest rates impact commercial real estate:

- Prices may come down. In recent years, CRE assets have been trading at all-time highs. It was not uncommon to see deals trading at or below a 3-cap, depending on property type and market. In a low-interest-rate environment, investors are willing to pay more for an asset. As interest rates rise, investors need to pay less for the property to achieve the same numbers. This can have a cooling effect on the market.

- Transaction activity may slow. As interest rates rise, some would-be buyers will remain on the sidelines, afraid of overpaying for a property given the high cost of debt. Meanwhile, would-be sellers may decide to hold off on selling until market conditions once again improve in their favor.

- Investors may look elsewhere. With interest rates on the rise, investors will begin looking at their alternatives. In an inflationary environment, some deals may not offer a compelling risk-adjusted return relative to other investments. For example, one consequence of rising inflation is that the yields on U.S. Treasury bonds are increasingly rising. Properties that were trading at a 3-cap become less compelling if the rate on 10-Year Treasury bonds is 2.5 percent, which they are today. In other words, the risk-adjusted returns on CRE should be higher than other investment types. If higher interest rates mean they are not, some people may decide to invest elsewhere until conditions change. The flip side of this is that the 2.5 percent “risk free rate” of a 10-Year Treasury bond does not offer any upside or future appreciation, while solid long term real estate deals operated by experienced managers can still offer upside. This is particularly the case in a high interest rate environment in which rents on multifamily assets generally benefit from inflation.

Should CRE Investors Panic? No – At Least, Not Yet.

While CRE investors should certainly monitor the interest rate environment, it is important to understand that the Federal target rate is not the be all, end all.

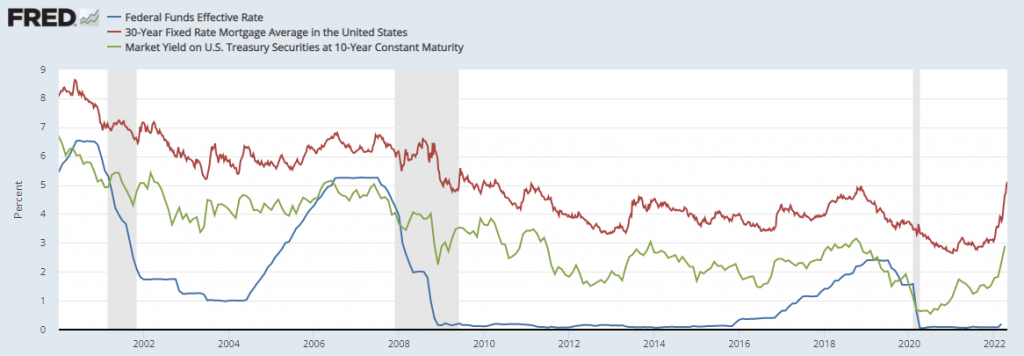

In fact, many would argue it’s the wrong indicator to be following. Instead, investors should be paying close attention to what’s happening to yields on 10-Year U.S. Treasuries.

The chart below highlights how changes in the Fed’s target rate (the blue line) don’t actually have a dramatic impact on mortgages (red line). Instead, there is a stronger correlation between the yields on 10-Year Treasures (green line) and mortgages.

The yield on Treasuries is certainly influenced by the Fed’s target rate, but it is also influenced by other factors such as the stock market and geopolitical events (e.g., the war in Ukraine). Given today’s economic and political environment, it would not be a surprise to see Treasury yields increase further, therefore pushing mortgage rates up in turn.

That said, interest rates, though they are on the rise, remain dramatically lower than they were in decades past. Using the same chart above, we can see that mortgage interest rates were close to 9 percent in the early 2000s. And remember, mortgage interest rates were upwards of 18 percent in the early 1980s. We are nowhere close to that, even if interest rates “rapidly” rise.

Some sectors, such as multifamily, will continue to outperform other asset classes even amid rising interest rates. Any downward pressure caused by rising mortgage rates should be counteracted by unfettered demand for housing. Investors continue to pour record amounts of capital into multifamily and for now, this shows no signs of slowing down. Rising interest rates are generally correlated with improving economic conditions, and as the economy improves, landlords will be able to push rents to combat higher priced debt. Meanwhile, office, retail, and hospitality properties will be bolstered by a generally improving economy.

While the Fed’s interest hikes certainly draw a lot of attention, it is important to put this news in the context of other market factors driving the CRE landscape. On the whole, the CRE market remains strong. At HLC Equity, we continue to pay close attention to the debt markets as interest rates rise and act defensively to preserve our investors’ capital. Interested in learning more? Contact us today.

The commercial real estate industry uses a lot of lingo. For instance, one of the most popular ways to distinguish properties is by their “class” rating. Assets are typically classified as either Class A, Class B, or Class C properties. This is true across all product types, regardless of whether it’s in reference to office, multifamily, retail, or industrial real estate.

In this article, we look at the distinguishing characteristics of Class A vs. Class B vs. Class C properties. Any prospective investor will want to learn this classification system so that they understand what type of product they’re investing in when they do.

Features of Class A Properties

Although there is no universally-accepted definition of a Class A (or Class B or Class C) properties, most in the industry consider Class A buildings to be newer with higher-quality finishes, amenities and accessibility. Class A properties tend to be located in the urban core, and oftentimes have their own brand or lifestyle associated with them.

Class A properties tend to be extremely desirable, investment-grade properties with the highest quality construction and workmanship, materials, systems and amenities. They will usually have best-in-class property management, as well.

Class A properties are also distinguishable for the tenants they attract. Most Class A properties will be occupied by prestigious, highly credit-worthy tenants that are willing to pay above-average rental rates. Class A properties are frequently bought and sold by national and international investors, including institutional investors who are willing to pay a premium for quality assets.

The desirability of Class A buildings means that they provide more liquidity than Class B or Class C properties. In other words, there is enough consistent interest in Class A properties that an investor can expect to have an easier time selling the property than if they were trying to sell a Class B or Class C property in the same market.

For these reasons, Class A properties are considered one of the “safest” additions to an investor’s portfolio (but conversely, offer some of the lowest returns in exchange for this lower risk profile). They’re also among the most expensive to purchase.

Features of Class B Properties

A Class B real estate tends to offer more utilitarian space with fewer amenities than one would find in a Class A building. It will typically have ordinary design and structural features, with average interior finishes, systems, and floor plans. The systems will be in adequate condition and the property will be structurally sound, but not overwhelmingly impressive.

The maintenance, management, and tenants in a Class B property are considered good (but not necessarily great). Tenants may be less established, have lower credit, or may be unable to sign longer-term leases. Therefore, while Class B buildings tend to attract broad interest among a wide range of users, the rents these tenants are willing to pay tends to be less than what Class A properties can command.

Class B properties are often considered more of a speculative investment than their Class A counterparts. Class B properties will occasionally attract attention among national investors, but most investors tend to be local to the marketplace.

While Class B properties tend to be considered a “riskier” investment than Class A properties, there are still several benefits to adding a Class B building to your portfolio. Namely, well-located Class B properties can generally be purchased at a lower price (and therefore, have a lower barrier to entry), and can be renovated to Class A condition over time. As building improvements are made and leases turn over, the new owner can increase rents and improve the tenant mix. With thoughtful value-add strategies, an investor can realize greater returns through Class B properties than they might be able to achieve by investing in Class A buildings in the same market.

Features of Class C Properties

Class C buildings can be highly lucrative for those with a solid investment strategy, but these properties are certainly not without their risk. In fact, Class C properties are considered the riskiest of the three property classes featured here today.

One of the reasons for the additional risk is that these buildings are generally older (20+ years) and in need of substantial renovation. Many will show visible signs of deterioration, such as overgrown landscaping or crumbling building facades. These properties, because they are older, will usually include few, if any, on-site amenities.

Compounding the risk is the fact that Class C buildings tend to be located in less desirable locations. They may be farther from major employment centers and/or in areas with high crime and few neighborhood amenities. Often, those who occupy Class C buildings do so only because they are more affordable than the alternatives.

Class C properties, however, offer the potential for the highest cash flow out of these three property classes. This cash flow is hard-earned, though, given how management-intensive these buildings can be.

Primary Indicators of Property Class

There are several factors that affect a property’s classification, including location, the age of a building, property condition, amenities and occupancy. These factors should be considered generalizations, as there are almost always exceptions to each of the “rules” below.

- Location: A property’s location is one of the biggest driving factors of its classification. As noted above, Class A properties tend to be the most well-located. These properties will have easy access to major employers, hospitals, universities, and arts and cultural amenities including retail and restaurants.

Class B and Class C properties are generally in less desirable neighborhoods. Again, this is not always the case. A Class B or Class C property – whose classification is instead driven by its age, condition or lack of amenities – may have an excellent location but the building itself otherwise leaves much to be desired.

- Age of Building: Class A buildings tend to be newer (often, new construction), whereas Class B and Class C properties are usually older. Class C properties will usually be 20-30+ years old.

However, another exception to this “rule.” An older building, such as a historic property, can still earn Class A status if it meets the other criteria listed here. Older buildings are often gut renovated to include high-end finishes and other amenities akin to their newly-constructed peers.

- Property Condition: A property’s condition is one of the leading factors of its class. A property that has been fully renovated and upgraded with high-end finishes is more likely to achieve Class A status than a property that is old, weathered and in need of both cosmetic and structural repairs. As a result of property condition, Class A and B properties tend to need less maintenance than Class C buildings.

- Amenities: Class A properties will usually offer robust amenities. For example, at a multifamily property, this could mean an on-site fitness center, media room, concierge, underground or otherwise covered parking, outdoor pool, doggy daycare and more. The larger the apartment community, the more robust the amenities will tend to be. Class B and Class C properties usually have fewer, if any, amenities to offer residents.

- Occupancy: Occupancy is a key factor in property class. Class A properties tend to have high occupancy rates, whereas Class C properties will usually have disproportionately high vacancy rates (with Class B properties falling somewhere in between). The tenants who occupy Class A buildings will generally be more established, higher earning, and will boast stronger credit profiles than those who lease Class B or C properties.

People often ask whether it is “best” to invest in Class A, B or C properties. There is no right or wrong answer. Any of them can be an excellent investment opportunity depending on the terms of the deal and the investment strategy. Any investor will want to consider their own risk tolerance, need for liquidity, and portfolio diversity when considering deals among different property classes.

Many investors will refer to a project’s “equity waterfall,” which at first glance, may seem complicated or difficult to understand. In reality, the equity waterfall simply refers to the manner in which cash flow and other profits are returned to investors.

What makes waterfalls complex is that they can be structured in countless ways. Understanding the structure is important for any passive investor who is considering investing in a commercial real estate deal.

Understanding What’s Behind the Name

At first glance, the term “waterfall” might not be one you’d expect to see applied in commercial real estate. But a deeper look behind the name reveals why this term is, indeed, quite appropriate.

The term “waterfall” stems from the idea that cash flow from an investment flows to different parties in numerous ways. The profits gather in a “pool” until that pool is full, at which point the profits spill over to the next pool of investors in a tiered fashion. It’s just like when water gathers at the top of a waterfall and then, after reaching a certain threshold, spills over to a pool below, sometimes multiple times.

Just as nature’s waterfalls can have numerous pools below, so too can real estate waterfalls.

Common Equity Waterfall Terms Explained

Before getting into an example, it’s helpful to understand a few terms that are often used when discussing commercial real estate equity waterfalls. Understanding these terms will help you understand why certain tiers of a waterfall function the way they do.

- Return Hurdles: A return hurdle defines the rate of return that must be achieved before the cash flow can flow from one tier to the next. Most waterfalls have multiple return hurdles. These return hurdles are often based on an internal rate of return (IRR) or equity multiple.

- Preferred Return: The preferred return, or “pref,” refers to the return certain investors will earn before other investors (e.g., common equity investors) begin earning their returns. Depending on how an investment is structured, there may or may not be a preferred return offered.

- Lookback Provisions: When equity waterfalls distribute cash flow prior to the disposition of the asset, the deal will typically contain what’s known as a “lookback provision”. Essentially, if the limited partners don’t get their minimum agreed upon rate of return after disposition, the general partner (e.g., the sponsor) is required to give up a portion of the cash flow they collected prior to the sale. This lookback provision is one of the key ways to motivate the GP to meet – if not exceed – return projections.

- Catchup Provisions: Whereas some equity waterfalls are structured to distribute cash flow to different parties during the course of the deal, other equity waterfalls are structured with what’s known as a “catchup provision.” A catchup provision stipulates that the limited partners will receive 100% of the deal’s cash flow until an agreed upon rate of return is met. After achieving that rate of return, all proceeds will then go to the general partner until they’ve received a specified rate of return.

A Common Equity Waterfall Structure

The most basic equity waterfall typically has four tiers. As described above, the first tier is where the cash flow builds into a pool—once that pool overflows, the profits flow down to the next tier.

Tier I. Return of Capital: In this tier, 100% of cash flow distributions go straight to the LPs.

Tier II. Preferred Return: All cash flow is distributed to the LPs again until a preferred return on their investment is achieved. The preferred return is sometimes referred to as the “hurdle rate” and can range from 7-10% or more.

Tier III. Catch-Up: This is where the catch-up provision comes into play. All distributions in this tier go to the GP until they achieve a certain percentage of the profits.

Tier IV. Carried Interest: At this point, the GP receives a disproportionately larger share of the cash flow distributions in the form of promotes.

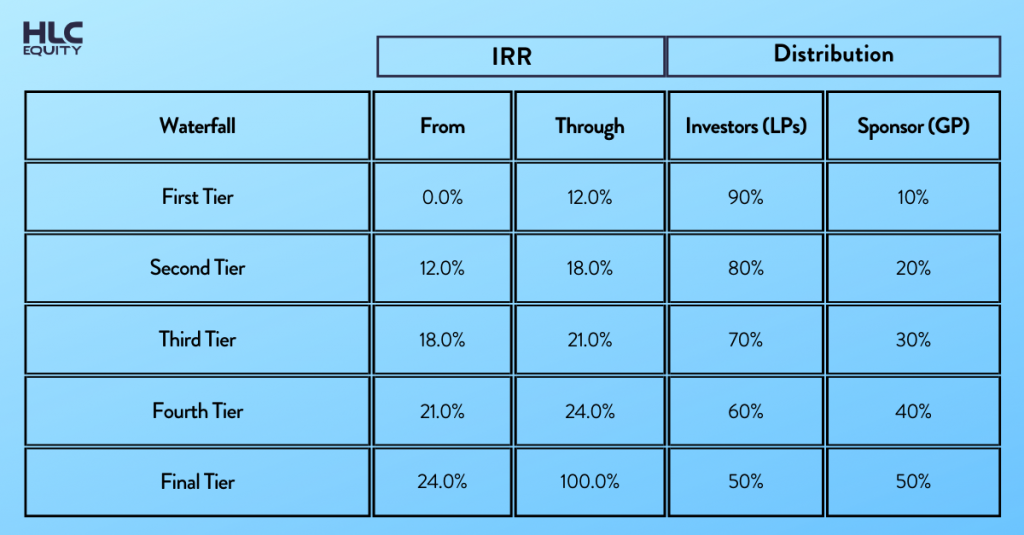

A Sample Equity Waterfall

Equity waterfalls can be structured in many ways. Here is a very basic example in which the LPs have invested $4 million (90% of total equity) and the GP has invested $400,000 (10%). Here’s how a basic waterfall might be structured in this case:

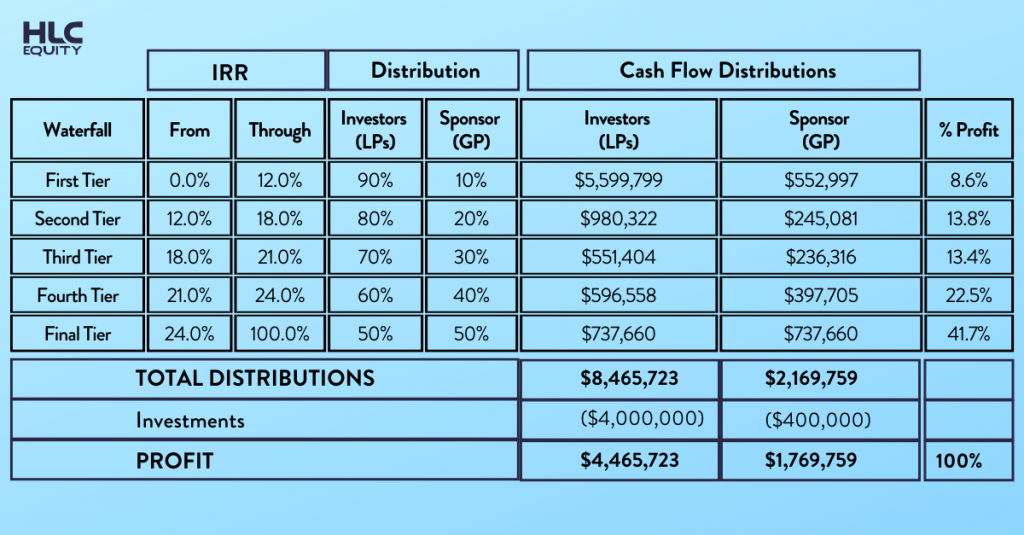

And here is how that might take effect, in practice:

As you can see in this example, the LPs have more invested in the deal and therefore, earns a preferred rate of return until a certain IRR threshold is met. Once that IRR threshold is met, the GP begins to earn a disproportionately larger share of the profits in the form of “promote”. These promotes are intended to motivate the sponsor to work diligently on the investors’ behalf, essentially earning success fees if they exceed original return expectations.

Real estate equity waterfalls are not easy to grasp, even for those who have years of experience in the industry. They can be filled with complicated tiers, returns, and provisions that are all interconnected to support a structure of uneven distributions of profit from a specific project. Breaking down the different features of an equity waterfall can provide investors with a clearer understanding of how a project’s returns will be distributed to whom and when.